actuarymath

-

Content Count

44 -

Joined

-

Last visited

Posts posted by actuarymath

-

-

I am in insurance industry and I am interested in pet insurance.In Japan some insurers launched on pet insurance but some of them are said to use the foreign (outside Japan) statistics.If some of you know the statistics of pet insurance or those of pet sickness and injuries, would you teach me where the statistics are?

-

Would someone teach me the lauguage usage in Xisto free web hosting?

In the TOS(terms of services) of Xisto free web hosting,

http://forums.xisto.com/topic/5769-terms-of-service-and-acceptable-use-policy/

"All websites must be in English to qualify for free hosting. We do this to ensure that Accounts are legal and have permissable contents."

But I found at a review site

http://forums.xisto.com/no_longer_exists/

that

"They are amazing. Non-English sites ARE allowed, except you have to have an English overlook page detailing your site so they know what it is about."

Which would be right? -

Awesome find, I know there's tons of sites like this one which not only do blogs but websites to. But this one specializes in blogs, which is quite a good unique selling point to have.

I'd love to know how they can determine what makes one website more expensive then another. I mean if one blog only had one page and on that page was the meaning of life. Then another website had 1,000 pages all about some random guys life, how can this site determine which has more value to it?

Okay, I may of gone over the top there, but you get my idea. If one blog's information is more important then another's who simply has more content, how can this website tell that? I've obviously had to much to think about this.

Forbez

Thank you for your reply.

As you will find when you visit the site

http://www.business-opportunities.biz/2005/11/16/how-much-is-my-blog-worth-now/

It seems to depend on

http://technorati.com/

I think the points would depend on the linkage from technorati.

I tried on some (Japanese) blogs I know but many of them which had more posts than mine gained NO points.

This may be because the blogs have no linkage from technorati.

-

I've found a site as below that shows you the "value" of your blog.

http://www.business-opportunities.biz/2005/11/16/how-much-is-my-blog-worth-now/

My blog

http://d.hatena.ne.jp/actuary_math/

is worth $1,129.08.

-

wwilliamsinformative post... is this anywhere in FAQs if not i think it would make a good addition to them

Thank you very much for your comment.

I also think FAQs would contain such information about SSH.

By the way will you tell me the below thing if you know?

I understand once we are hosted the points correspond to the survival days (1 point=1 day survival).

But I am afraid that my survival days seem to decrease more faster than 1point/1day.

Do you know the rule of "decreasing survival days"?

-

Thank you for your reply.We do not allow SSH on Qupis at all

Only trap and paid members are given SSH.

Only trap and paid members are given SSH.

I have thought that Qupis allows ssh because it has SSH menu.

I would have not been confusued if your Qupis cpanel menu have not shown the SSH menu!

-

Hello Actuary,

Thank you for opening a topic regarding SSH here. We do not offer SSH by default in our packages, SSH is granted to members only after they send an email request regarding the same. Now if you wish to have SSH enabled on your account you need to send an email to :-

support(at)Xisto(dot)comsupport(at)Xisto(dot)comThe content of your request should be in the below format :-TITLE : Request for SSH on sub domain actuary.trap17.com

MAIN POINTS :

Your Forum UsernameForum PasswordCpanel UsernameCpanel PasswordReason as to why you need SSHYour current Credit AmountOnce you send the above details, OpaQue or BuffaloHelp will review the application and SSH will be enabled depending on your forum behavior and email request. If you have any further doubts or queries you may add them in the same request email.

Thank you very much for your reply.By the way is this same as Qupis?

That is, do I have to send an application email to qupis support like the above format to use SSH on Qupis?

(If I have to post the matter at the Qupis corner, please indicate me so)

-

I was allowed to have an account

http://forums.xisto.com/no_longer_exists/

and I would like to use SSH access that I believe is a salespoint of Xisto.

At the video tutorial, it seems that we can use Java SSH but I could not find the icon about it.

And I used the PuTTy and tried to connect but I was refused.

Of course I have authorized the public key at my cpanel.

My setting was as follows.

host name:actuary.trap17.com

account name:actuary

password:(password I use at cpanel)

Port No 22

If I made some mistakes, will some of you please let me know? -

I believe that how few we consider the "parameter risk".Suppose that the probability of occurring a accident is P (0<P<1).For N polices, the probability of occurring n accidents isN_C_n * P^n * (1-P)^(N-n)(where N_C_n means the combinatorial number which is chosen n things form N things)Suppose that the p.d.f.(probability density function) of the prior distribution is g(p),f(p),the p.d.f. of the posterior distribution by Bayes' theoremwill be proportional to P^n * (1-P)^(N-n) *g(p)(because N_C_n is a constant which has no relations with p)Now if the prior distribution is a uniform distribution, that is g(p)=1(0<p<1)f(p) is proportional to P^n*(1-P)^(N-n)soP follows to B(n+1,N+1)(beta distribution).

-

I am running the blog about "Examination to be Actuaries"

at

http://d.hatena.ne.jp/actuary_math/

The blog is written in Japanese, but I will introduce you some articles by translation in English.

...

Then I will introducehttp://d.hatena.ne.jp/actuary_math/20080705

by translating into English.

The following question is a little alternation from one seen in the past exam.

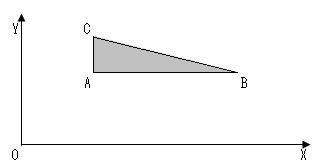

Question

In the above picture, AB is parallel to x-axis and AC is parallel to y-axis.

(X,Y) are 2 dimensional random variables which follow uniform distributions on triangle ABC.

The correlation coefficient X,Y rho(X,Y) is [ ]

(fill in the blank)

----------

In this question neither the position (x,y) of A the nor the length of AB or AC are not given.

So some of you may begin to present the position and the length as some variances.

However, we will make the perceptional change.

That is

"The answer is the same even if the position (x,y) of A the or the length of AB or AC.

Therefore, we can let them whatever we like.」(*)

So we will let A(0,0),B(1,0),C(0,1).

E(X)=E(Y)

=2{\int_0^{1} xdx \int_0^{1-x}dy}

(I will mean "\int_a^b" by integral from a to b as TEX usage)

=2 \int_0^1 (x-x^2)dx

=2(1/2 - 1/3)=1/3

E(X^2)

=2 \int_0^1 x^2dx \int_0^{1-x}dy

=2 \int_0^1 (x^2-x^3)dx

=2(1/3 - 1/4)=1/6

V(X)=V(Y)

=E(X^2)-{E(X)} ^2

=1/6-(1/3)^2=1/18

E(XY)

=2 \int_0^1 xdx \int_0^{1-x} ydy

= \int_0^1 x(1-x)^2 dx

=\int_0^1 (x-2x^2+x^3) dx

=1/2 - 2/3+ 1/4=1/12

Cov(X,Y)

=E(XY)-E(X)*E(Y)

=1/12 - 1/3*(1/3)=- 1/36

rho (X,Y)

=Cov(X,Y)/sqrt{V(X)*V(Y)}

=(-1/36)/(1/18)=-1/2

(*)The ideas can be authorized as follows.

First we put the position of A is (a,b ) and the length of AB and AC are c and d respectively.

Then we put X'=(X-a)/c, Y'=(Y-b )/d

as rho (X,Y)=rho (X',Y')

(Because the correlation coefficient does not vary by addition, subtraction, multiplication and division of constants.)

In the original question A is the Original point(0,0) and the length of AB=a and AC=b were given.

But according to the above thought, we can easily find that the answers with a,b are all WRONG.

The idea can not be limited to the actuary examination, and to be applicable to all objective type examinations.

-

I am running the blog about "Examination to be Actuaries"

at

http://d.hatena.ne.jp/actuary_math/

The blog is written in Japanese, but I will introduce you some articles by translation in English.

Let's brgin with the use of the "elimination" this time.

(The oringinal url is

http://d.hatena.ne.jp/actuary_math/20080718

)

I think you often use naturally the method of "elimination" in other selection type questions and quizzes etc.

The problem below is taken up in the past exams.

(Question)

Let X,Y, and Z are independent random variables with uniform distributions of U(0,2), U(-1,1), and U(-2,0) respectively.

The probable density function(p.d.f.) of S=X+Y+Z is

[1] (-3 <= s <= -1)

[2] (-1 <= s <= 1)

[3] (1 <= s <= 3)

0 (otherwise)

(select the blanks [1] to [3] by the following choices (A) to (L) )

(A){(s+3)^2}/4

( B ){(s+3)^2}/8

( C ){(s+3)^2}/16

(D){(s-3)^2}/4

(E){(s-3)^2}/8

(F){(s-3)^2}/16

(G)(3+s^2)/4

(H)(3+s^2)/8

(I)(3+s^2)/16

(J)(3-s^2)/4

(K)(3-s^2)/8

(L)(3-s^2)/16

-----------------

This question can be solved by the compound of 2 or 3 random variables.

But the situation division is unexpectedly troublesome.

Here, we will squeeze the candidate of the answer is squeezed by the elimination without calculating like this.

If we choose without no thought than not choosing the same one twice

the number of the candidates are 1,320( permutations 12P3 ,that is selecting 3 in a row from 12).

However it is possible to narrow up to two candidates by the following discussion and only one remains with high possibility of the two. (It is actually the correct answer.)

1.

First of all, let us clear the first hurdle installed in the problem sentence.

We put X'=X-1 and Z'=Z+1 respectively.

The variables X',Y and Z' are the same and independent variables which follow uniform distributions U(-1,1).

Moreover, it is understood that the answer becomes symmetric because S=X'+Y+Z' and because U(-1,1) is symmetric distribution, too.

So, the combination of candidates of [1]-[3] are the following 3 pairs

(A)-(D),

( B )-(E)

and

( C )-(F)

And the candidates of [2] are the 6 choices from (G) to (L).

At this point, the number of the candidates becomes 3*6=18.

2.

Next,

We will use the fact that

"We get 1 when we integrate a probability density function (p.d.f.) where the value of the p.d.f is positive (in this case only with -3 <= s <=3)".

(i)

The integral from -3 to -1 of (A) is

\int_{-3}^{-1} \frac{(s+3)^2}{4}ds=[{(s+3)^3}/{12}]_{-3}^{-1}=2/3

(I mean \int_a^b f(x) dx and [F(x)]_a^b by the integral f(x) from a to b and F( b )-F(a) respectively)

So is the integral of (D) from 1 to 3 (because (A) and (D) are symmetric)

We get the integral from -3 to -1 of ( B ) (= the integral from 1 to 3 of (E) ) and the integral from -3 to -1 of ( C ) (= the integral from 1 to 3 of (F) ) are respectively 1/3 and 1/6

(ii)

We get the integrals of (G) - (H) from -1 to 1 are respectively

(G) 5/3,

(H) 5/6,

(I) 5/12,

(J) 4/3,

(K) 2/3

and

(L) 1/3

So

The candidates of three combinations of [1]-[2]-[3] are

(1)( B )-(L)-(E) (1/3 + 1/3 + 1/3 =1)

(2)( C )-(K)-(F) (1/6 + 2/3 + 1/6 =1)

Well, which of the 2 candidates is the correct answer?

When two graphs are drawn, they are

(1)

http://f.hatena.ne.jp/actuary_math/20080718194236

And,

(2)

http://f.hatena.ne.jp/actuary_math/20080718194235

respectively.

Here, the candidate (2) of which the graph is "Continuous" seems to be correct.

Because of the following proposition, it is actually correct.

(Proposition)

"Let X and Y are independent probability density functions f(x) and g(y) respectively which are almost everywhere continuous(*). At least one of the functions (f(x) and/or g(y)) is(are) bounded. So h(s),the probability density function of S=X+Y is continuous at all s"

(This proposition will proved at another moment because it is not easy. )

(*) I will not define "almost everywhere continuous." But even if it is discontinuous at limited points, the definition of "It is almost continuous everywhere" holds.

The point is that even if there are limited "discontinuous" points of f(x) and g(y) the h(s) is continuous for ALL points.

Therefore, by the "elimination" we can not set the combination of [1]-[2]-[3]

other than

( C )-(K)-(F).

Of course things do not go well like every time

But we can often narrow by the elimination.

Let us think the above question in another point of view ("central limit theorem")

(The original Japanese version is

http://d.hatena.ne.jp/actuary_math/20080722" target="_blank"> http://d.hatena.ne.jp/actuary_math/20080722 )

The notation of the central limit theorem will be seen in the below URL

https://en.wikipedia.org/wiki/Central_limit_theorem

But practically in the actuarial exam

"Central limit theorem"

can be regarded as "We can regard the distribution as a normal distribution."

In this question, as 3 distributions are compounded, the distribution can be regarded to be near the normal distribution.

The graphs of the normal distributions look like bell form.

(For example see

https://en.wikipedia.org/wiki/Normal_distribution

)

In this question

(1) The graph of the neighborhood of the mean value is regarded to (upward) convex.

So (G)-(I) are eliminated of the candidates of [2] because their graphs are concave (or downward convex).

(2) The graph is "gathered" to the center. That is the probability P(-1 <= s <=1 ) is larger than P(-3 <= s <=-1 )(=P(1 <= s <=3 ))

So (L) is eliminated from (J)-(L),the rest of (1) because the integral of (L) from -1 to 1 is 1/3.

Then (J) and (K) are remained but (J) is out of the question because the integral of (L) from -1 to 1 is 4/3 which is larger than 1.

Then the candidate of [2] is determined to (K).

The sides candidates [1] and [3] are set to be the integrals equal to 1/6.So are ( C ) and ( F ).

This method can be used when we verify the answer normally calculated.

-

In the last post I left proof of a proposition.So I will prove it as below.We must use the Lebesgue's integral theory to prove the proposition.PropositionSuppose that X and Y are independent random variables with probable density functions f(x) and g(y) respectively.And suppose that f(x) and g(y) are continuous almost everywhere, and that a least one of f(x) and g(y) is bounded.Then h(s),the p.d.f. of S=X+Y is continuous at ANY real number s.ProofAs h(s)=\int f(s-y)g(y)dy=\int f(x)g(s-x)dx(In the above formula "\int" means integral from -infinity to +infinity.)it is sufficient that we suppose that f(x) is bounded.That is there is a positive real number K that f(x)<K for all x.And it is sufficient for us to prove that for any sequence {s_n} that converges to s\int f(s_n-y)g(y)dy =h(s)Note thatf(s_n-y)g(y) <= K*g(y)and that\int K*g(y)=K*1=K<+infinity(because h(s)=\int g(y)dy=1)On the other handfor almost any yf(s_n-y)g(y) converge to f(s-y)g(y).(because f(x) and g(y) are continuous almost everywhere) So we get\int f(s_n-y)g(y)dy =h(s)by dominated convergence theorem(or Lebesgue's convergence theorem)q.e.d.

-

I am running the blog about "Examination to be Actuaries"

at

http://d.hatena.ne.jp/actuary_math/

The blog is written in Japanese, but I will introduce you some articles by translation in English.

Let's brgin with the use of the "elimination" this time.

(The oringinal url is

http://d.hatena.ne.jp/actuary_math/20080718

)

I think you often use naturally the method of "elimination" in other selection type questions and quizzes etc.

The problem below is taken up in the past exams.

(Question)

Let X,Y, and Z are independent random variables with uniform distributions of U(0,2), U(-1,1), and U(-2,0) respectively.

The probable density function(p.d.f.) of S=X+Y+Z is

[1] (-3 <= s <= -1)

[2] (-1 <= s <= 1)

[3] (1 <= s <= 3)

0 (otherwise)

(select the blanks [1] to [3] by the following choices (A) to (L) )

(A){(s+3)^2}/4

( B ){(s+3)^2}/8

( C ){(s+3)^2}/16

(D){(s-3)^2}/4

(E){(s-3)^2}/8

(F){(s-3)^2}/16

(G)(3+s^2)/4

(H)(3+s^2)/8

(I)(3+s^2)/16

(J)(3-s^2)/4

(K)(3-s^2)/8

(L)(3-s^2)/16

-----------------

This question can be solved by the compound of 2 or 3 random variables.

But the situation division is unexpectedly troublesome.

Here, we will squeeze the candidate of the answer is squeezed by the elimination without calculating like this.

If we choose without no thought than not choosing the same one twice

the number of the candidates are 1,320( permutations 12P3 ,that is selecting 3 in a row from 12).

However it is possible to narrow up to two candidates by the following discussion and only one remains with high possibility of the two. (It is actually the correct answer.)

1.

First of all, let us clear the first hurdle installed in the problem sentence.

We put X'=X-1 and Z'=Z+1 respectively.

The variables X',Y and Z' are the same and independent variables which follow uniform distributions U(-1,1).

Moreover, it is understood that the answer becomes symmetric because S=X'+Y+Z' and because U(-1,1) is symmetric distribution, too.

So, the combination of candidates of [1]-[3] are the following 3 pairs

(A)-(D),

( B )-(E)

and

( C )-(F)

And the candidates of [2] are the 6 choices from (G) to (L).

At this point, the number of the candidates becomes 3*6=18.

2.

Next,

We will use the fact that

"We get 1 when we integrate a probability density function (p.d.f.) where the value of the p.d.f is positive (in this case only with -3 <= s <=3)".

(i)

The integral from -3 to -1 of (A) is

\int_{-3}^{-1} \frac{(s+3)^2}{4}ds=[{(s+3)^3}/{12}]_{-3}^{-1}=2/3

(I mean \int_a^b f(x) dx and [F(x)]_a^b by the integral f(x) from a to b and F( b )-F(a) respectively)

So is the integral of (D) from 1 to 3 (because (A) and (D) are symmetric)

We get the integral from -3 to -1 of ( B ) (= the integral from 1 to 3 of (E) ) and the integral from -3 to -1 of ( C ) (= the integral from 1 to 3 of (F) ) are respectively 1/3 and 1/6

(ii)

We get the integrals of (G) - (H) from -1 to 1 are respectively

(G) 5/3,

(H) 5/6,

(I) 5/12,

(J) 4/3,

(K) 2/3

and

(L) 1/3

So

The candidates of three combinations of [1]-[2]-[3] are

(1)( B )-(L)-(E) (1/3 + 1/3 + 1/3 =1)

(2)( C )-(K)-(F) (1/6 + 2/3 + 1/6 =1)

Well, which of the 2 candidates is the correct answer?

When two graphs are drawn, they are

(1)

http://f.hatena.ne.jp/actuary_math/20080718194236

And,

(2)

http://f.hatena.ne.jp/actuary_math/20080718194235

respectively.

Here, the candidate (2) of which the graph is "Continuous" seems to be correct.

Because of the following proposition, it is actually correct.

(Proposition)

"Let X and Y are independent probability density functions f(x) and g(y) respectively which are almost everywhere continuous(*). At least one of the functions (f(x) and/or g(y)) is(are) bounded. So h(s),the probability density function of S=X+Y is continuous at all s"

(This proposition will proved at another moment because it is not easy. )

(*) I will not define "almost everywhere continuous." But even if it is discontinuous at limited points, the definition of "It is almost continuous everywhere" holds.

The point is that even if there are limited "discontinuous" points of f(x) and g(y) the h(s) is continuous for ALL points.

Therefore, by the "elimination" we can not set the combination of [1]-[2]-[3]

other than

( C )-(K)-(F).

Of course things do not go well like every time

But we can often narrow by the elimination. -

I owned a Japanese blog at

http://d.hatena.ne.jp/actuary_math/

Once I posted taking about pension mathematics at

http://d.hatena.ne.jp/actuary_math/20080819

Now I translate it into English as follows because it will somehow server those who studies pension mathematics.

Because I think that I become wrong perhaps if it digs more than this down about corporate pension accounting/retirement benefit accounting because it is unprofessional, could you pardon the respect?----I will obtain the questioner's consent and publish because the question concerning the pension mathematical principle is received from the reader of the blog, and it did the round trip letter several times (In E-mail).

It would be greatly appreciated if it could help you because there might be similar doubt.

leaning though it has been passed by the life insurance mathematical principle and there is knowledge at a constant level the questioner.

< points of concern >

(1)I must consent for the examination of not the specialist of the pension mathematical principle but the pension mathematical principle and ten years or more from now it is ahead.

(Though the text etc. of the pension mathematical principle have been reviewed because the actuary examination has been guided afterwards. )

(2)Moreover, I must pardon digging corporate pension accounting/retirement benefit accounting of corporate pension accounting/retirement benefit accounting because of unprofessional it down though it writes at the end of a series of communication.

(3)An unrelated part to the question like the greeting etc. is omitted. Moreover, it changes within the range where the meaning of a so-called platform dependent character like the encircled number etc. etc. is not changed.

Question 1

Frequently I am sorry. Though I would like you to teach when it is understanding.

As for the comprehensive insurance open fee type of the pension mathematical

principle, it is.

There are four patterns in the comprehensive insurance open fee type when the

system is introduced. (F_n=0 when introducing it)

(1)It supplies to the retiree, and the work period of the past is

totaled.

P_n^{(1)}=\frac{S^p+S^a+S^f-F_n}{G^a+G^f}

(\frac{x}{y}=x/y as is same as follows)

(2)It doesn't supply even to the retiree, and the work period of the

past is not totaled.

P_n^{(2)}=\frac{S^a+S^f-F_n}{G^a+G^f}

(3)The work period on the past of the insurant of in service is not

totaled.

P_n^{(3)}=\frac{S^a_{FS}+S^f-F_n}{G^a+G^f}

(4)The object person of the supply is limited only to the insurant in

the future.

P_n^{(4)}=\frac{S^f-F_n}{G^a+G^f}

It is.

Q1 . Is to regularity this pattern?

As well as P_n^{(1)} it when it becomes regular Is it P_n=\

frac{S^p+S^a+S^f-F_n} {G^a+G^f}?

Or, is the pattern of (1) ?(4) applied even if becoming regular?

By the way,

In the 13th line at the page 107 in

http://www.su-jine.net/

I saw "the premium will be also applied as same as that was fiexd at the beginning."

and I thought it was not as same as P_n^{(1)}.

Nevertheless in the formula (5.87) at the page 108 in the same book P_n^{(1)} was written.

So I was very confused.

Q2 . V of (1)-(4) is not described in the textbook, and the expression of V is not understood and it embarrasses it.

Respectively

Will it be V=S^p+S^a+S^f-P(G^a+G^f) (As for (1)-(4), P is P_n^{(1)}-P_n^{(4)} respectively)?

Or,do it become

(1)V_n=S^p+S^a+S^f-P_n^{(1)}(G^a+G^f)

(2)V_n=S^a+S^f-P_n^{(2)}(G^a+G^f)

(3)V_n=S^a_{FS}+S^f-P_n^{(3)}(G^a+G^f)

(4)V_n=S^f-P_n^{(4)} (G^a+G^f)?

By the way, when it can be taught how to do F, it is very welcome.

Answer 1

>saying that "(close type) aggregate cost method" (text p76-p79 (The textbook of IAJ (the institute of actuaries of Japan) is indicated: It is the same as follows))

When "Comprehensive insurance open fee method" (text p87-p91) is confused, it is feared.

"Close type comprehensive insurance fee method" is only indicated in case of "Aggregate cost method".

Insurance is not defined by "Progression" like F_n about "Type of open" comprehensive insurance fee method in the book (text , http://www.su-jine.net/ and http://www.su-jine.net/) for me, and insurance steadies.

Or, a page concerned is scanned if it is possible to do if it is a book other than and there is such a description and it is welcome when sending it.

>

http://www.su-jine.net/

As for "The premium provided when the system of the premium is introduced will be applied regardless of the passage in fiscal year", insurance is thought by the 13th line of P107 of the book > that it means the insurance decided once is applied every year (Special insurance is none) during year by each of the four patterns though differs.

The constant insurance is different according to each pattern.

http://www.su-jine.net/

Because this value is different by each pattern, insurance is different though it drinks and there is ^{o}F about the formula (5.87).

Reserve fund = liability reserve (If you do not think about the profit loss

from the difference of quotation profit etc.) concrete (stationary state)

can be requested by applying limit equation C+d*F=B.

Question 2

Q1.

http://www.su-jine.net/

There is insurance of the stationary state of the comprehensive

insurance open fee type according to drinking p108 when it is

expressible like expression (5.87) ^{o} P=\frac{S^p+S^a+S^f-^oF} {G^a+G^f}.

Possibly

Insurance is thought to mean the insurance decided once is applied every year (Special insurance is none) during year by each pattern of four > though differs.

The explanation thinks that it doesn't attach.

Does it settle down in one pattern four patterns in the stationary state?(Do it become an expression (5.87) momentarily became regular?)

Q2.

> can be requested by applying limit equation C+d*F=B.

What meaning is of the profit loss from the difference of quotation profit etc. not to think if and > profit loss from the difference of quotation profit of the point etc. are not thought when and F=V are approved?

Will F=V be mean no regular approval if the thing doesn't advance to the last according to the assumed interest rate and the assumed rate of mortality when F and V are calculated?

Answer 2

The insurance of the stationary state of the comprehensive insurance > open fee type is {} ^{o} expression (5.87) > P=\frac{S^p+S^a+S^f-^oF} {G^a+G^f} It is when expressible like >.

...>.. possibly>

> Insurance is thought to mean the insurance decided once is applied every year (Special insurance is none) during year by each of the four patterns though differs.

I think that the explanation > doesn't attach.

Does it settle down in one pattern the pattern of four > in the stationary state?>

(Do it become an expression (5.87) momentarily became regular?)

Four patterns are not to settle down in one.

(5.87)^{o} P is also different differing in ^{o} F four patterns though it peels off and it is writing by the expression) Thus, it does.

Concretely,

It supplies to > (1) retiree, and the work period of the past is

totaled.

^{o}F=0

It doesn't supply even to > (2) retiree, and the work period of the

past is not totaled.

^{o}F=S^p

The work period on the past of the insurant of in service of > (3) is

not totaled.

^{o}F=S^p+S^a_{PS}

The object person of > (4) supply is limited only to the insurant in

the future.

^{o}F=S^p+S^a

Thus, it does.

What meaning is not to think about > profit loss from the difference of quotation profit etc.

Will F=V be mean no regular approval if the thing doesn't advance according to the assumed interest rate and the assumed rate of mortality when F and V are calculated to the last ?

That.

If the thing doesn't advance according to the assumed interest rate

and the assumed rate of mortality and special insurance is not

received, unsavings debt U=V-F (text p72) is caused.

Question 3

Q.However, only one point

If > special insurance is not received, unsavings debt U=V-F (text p72) is caused.

The collection of special insurance that it is a point is understanding that the past service liability is lost. However, I do not think that there is actually entering of cash.

The one that F is cash (Because it is F=0 and (F_n+C) (1+i) - B=F_{n+1} at the first year) in my understanding reserved with the company, and it is necessary to save the same amount as V.

Moreover, when piling up when the past service liability (henceforth PSL) is introduced in pension system, and matching to V, amount insufficient in V doesn't pile up PSL. PSL will be adjusted to 0 during the future. It is light understanding.

When system is introduced if it is assumed PSL=100 when pension system is introduced in a word, and redeems it in ten years (Hereafter, when writing by the sort).

|[F] 100|[PSL] 100|

In one year

|[PSL] 100/10=10|Special insurance 10|

Near special insurance becomes insurance without the proof of cash.

Then, I think that it is not cash from which F is reserved with

the company.

Is understanding to my F wrong?

Q2 . moreover, why though it is a relating story might is Fackler's reflexive type when there is PSL different in F and V like (F_n+C^n+C^s) (1+i) - B=F_{n+1} and \ (V_n+C^n) (1+i) - B=V_{n+1}, etc.

(In C^n, standard insurance and C^s are special insurances;Because Japanese was not able to be used in diamond Lee's tex notation, the initial of normal and special was taken and it was written though it wrote in C signpost and C special Japanese in the quotation Shasoso original as n and s. )

(It asked and was written in the past of H13(14). )

Answer 3

>, only one point

>> If special insurance is not received, unsavings debt U=V-F (text p72) is caused.

The collection of special insurance is understanding that the past service liability is lost though it is a point >. However, I do not think that there is actually entering of cash.

The one that F is cash (Because it is F=0 and (F_n+C) (1+i) - B=F_{n+1} at the first year) in > my understanding reserved with the company, and it is necessary to save the same amount as V.

When piling up when the past service liability (henceforth PSL) is introduced in pension system, and matching to V, amount insufficient in > and V doesn't pile up PSL. PSL will be adjusted to 0 during the future. It is light understanding.

If it is assumed PSL=100 at > ,in a word, the pension system introduction, and redeems it in ten years (Hereafter, when writing by the sort) When > system is introduced.

|[F] 100|[PSL] 100|

In one year

|[PSL] 100/10=10|Special insurance 10|

It becomes > and special insurance becomes insurance without the

proof of cash.

I think > to be no cash from which F is reserved with the company

then.

Is understanding to > my F wrong?

PSL is not "Pile up" the one.

It recognizes it as a difference between the property (reserve fund)

and the debt (liability reserve).

When it is a presentation example(The liability reserve is not a tile. )

Balance sheet of system introduction

|Part of property|Part of debt|

|Cash (F) 0|Liability reserve (V) 100|

| |Part of net assets|

| |Loss money *100|

| |Part of debt and net assets|

| |100+*100=0|

Sort after one year

|Debit|Credit|

|Cash 10|Special insurance 10 (income account)|

(→ decreases loss money by this ten. )

Balance sheet after one year

|Part of property|Part of debt|

|Cash 10 (F)|Liability reserve (V) 100|

| |Part of net assets|

| |Loss money * 90|

| |Part of debt and net assets|

| |100+*90=10|

It becomes it.

> Q2 . It is (F_n+C^n+C^s) (1+i) - B=F_{n+1}, and moreover, > it is F, V, and Fackler's reflexive type when there is PSL is (V_n+C^n) (1+i) - B=V_{n+1} though it is a relating story why might do you differ like >?>

(In C^n, standard insurance and C^s are special insurances) Please see figure under > (It asked and was written in the past of H13(14)) text p73.

Special insurance doesn't enter the reflexive type of V because the difference between a supply present value and a standard insurance income present value is liability reserves.

On the other hand, because F is the entire reserve fund of the company, it is counted in including special insurance.

(It is thought assumed interest rate = actually that it is an interest rate in this problem, and when the interest rate is actually different from the assumed interest rate, ..only F.. is applied the interest rate actually. )

Question 4

Q1 . Indeed, special insurance has entering of cash. It became study very much.

Not piling up and PSL are that I whether be turning over and read ..PSL.. amount F in a word in a different way as Co loss money or surplus at the beginning of period.

On the other hand, because F is the entire reserve fund of the company, it ..Q2 ".. is counted in including special insurance. "

Because do you turn around to F?

By the way, a similar expression is to the question in the past of H17(2).

F at the time of of the end of fiscal year donates amount that in the under and the amount that falls below constant comparatively correspond to r with V as special insurance in a certain pension system at the time end of next year. This system is a stationary state.

Fiscal year..end..end..show..count..choose.It was, and ..period Hatshara.. donating special insurance in ..assumed interest rate i.. yield on investment j however had the problem of end of fiscal year. In this problem, is it a stationary state and does PSL exist at the beginning of period?The definition of the stationary state : though it must be V=F . However, the limit equation of F and V had been approved just like the stationary state why.

It wrote in (F+C^n- (1+i) (F+C^n- (1+j) + C^s=F = V C^s=r(V-F) and the answer.

(1+i) (F+C^n- (1+j) + C^s=F = V C^s=r(V-F) and the answer.

(Quotation ..Shasoso.. C^n and C^p are also the same on. )

Frequently I am sorry.

Answer 4

That ..the donation... entire pension funds the cash that has been

entered this > There is no place to which it goes besides pension

funds.

Because do you turn around to F?

F indicates pension assets by abbreviating Fund. Cash is one of the properties.

It is not though it actually thinks the part that has it like cash to be making to the minimum and a transfer to other properties (debenture and stocks, etc.) because the amount of the total changes only because contents of F change.

>, a similar expression is to the question in the past of No.(2) of the test in 2005.

F at the time of of the end of fiscal year donates amount that in the under and the amount that falls below constant comparatively correspond to r with V as special insurance in pension system with > at the time end of next year.

Choose the count type where this > system shows F at the end of fiscal year when it is a stationary state/fiscal year V at the end.

It was, and > ..period Hatshara.. donating special insurance in ..assumed interest rate i.. yield on investment j however had the problem end of fiscal year >.

Does > be a stationary state and have PSL in this problem at the beginning of period?

The definition of the stationary state : though it must be V=F .

The limit equation of F and V had been approved just like the stationary state ..>.. why. >

= V and C^s=r(V-F) of (F+C^n- (1+j) + C^s=F (F+C^n- (1+i) It wrote in > and the answer.

It is interpreted that "Regularity" indicates no straw at the new year and the end of the year here the amount of the property (F) and the debt (V).

In a word, the situation of making the state that the amount of money of F and V doesn't change at the new year and the end of the year with it had the unredemption debt with F<V "Regularity" is indicated. Of course, it can be said, the situation setting of this problem is "Problem" in such a meaning in keeping leave the state of liabilities in excess of assets (F<V), and no permission in the management of pension funds of the reality, and another who thinks by giving a clear-cut attitude purely and mathematically doesn't think that it is when put out as a problem.

First of all, though F

(a)Standard insurance and the supply go in and out in the property at

the new year and F+C^n-B.

(

Because this is operated with (1+j), (F+C^n- (1+j).

Š

Because special insurance enters here, the property at the end of

fiscal year is (F+C^n- (1+j) + C^s.

(d)Because this is "Regularity" state, it becomes (F+C^n- (1+j)

+ C^s=F in unison with the property at the new year.

I think that it can similarly catch V.

(However, insurance is standard insurance and the idea interest rate

is an assumed interest rate. )

When you base the above

(F+C^n- (1+j) + C^s=F (V+C^n- (1+i) = V I think that it

becomes C^s=r(V-F).

Question 5

>> That ..>... donate the cash that has been entered to entire

pension funds thisThere is no place to which it goes besides pension

funds.

Because do you turn around to F?

...>.. F indicates pension assets by abbreviating Fund. Cash is one of the properties.

There is no > though actually thinks the part that has it like cash to be making to the minimum and a transfer to other properties (debenture and stocks, etc.) because the amount of the total changes only because contents of F change.

Is it good in understanding of in the company but pension funds' judging from the correspondences of two sentences, changing into other financial assets and having it?

Moreover, will it be a past service liability and be this an equal sign in the textbook from the content of the previous mail though it ..since P177 "Past service liability" of the word.. is not used and the word surplus is used by it?

( Word PSL is used in http://www.su-jine.net/ )

Moreover, so good a pin and not coming are the correspondences with the retirement benefit accounting though it is a matter of the other day's sort. The difference may (it but the projected benefit obligation and the not same) with the quotation of pension assets is recognized as a difference in the mathematical principle calculation of the unrecognition (henceforth mathematical principle difference) in Hi, pension assets are piled up, and it increases. (sort: Pension assets | mathematical principle difference)And, it will recognize from next year of or at this season as a minus of the retirement supply cost cost, and actual cash is not donated. (sort: Pension assets | mathematical principle difference)Moreover, pension assets, the mathematical principle difference, and the projected benefit obligation are done in the net and it sums it up as a retirement supply reserve on B/S.

The example was appended. (By the way, the mathematical principle

difference doesn't swell in the interest in Hi. )

http://f.hatena.ne.jp/actuary_math/20080819072806

The retirement benefit accounting and the corporate pension accounting are

that.

Please teach if you know.

Answer 5

Is it good in understanding of in the company but pension funds' judging from the correspondences of sentences of two >, changing into other financial assets and having it?

I think it is good in such understanding.

Will it be a past service liability and be this an equal sign in the textbook from > and the content of the previous mail though it ..since P177 "Past service liability" of the word.. is not used and the word surplus is used by it?>

(http://www.su-jine.net/)

So good a pin and not coming are the correspondences with the retirement benefit accounting though it is a matter of > and the other day's sorts. The difference may (it but the projected benefit obligation and the not same) with the quotation of pension assets is recognized as a difference in the mathematical principle calculation of the unrecognition (henceforth mathematical principle difference) in Hi, pension assets are piled up, and it increases. (sort: Pension assets | mathematical principle difference)And, it will recognize from next year of or at this season as a minus of the retirement supply cost cost, and actual cash is not donated. (sort: Pension assets | mathematical principle difference)Moreover, pension assets, the mathematical principle difference, and the projected benefit obligation are done in the net and it sums it up as a retirement supply reserve on B/S.

As for the amount where it had worked before when pension system began literally, the past service liability is to mean there is a difference between the liability reserve and pension assets, and it becomes "Debt" originally without insurance because it supplies it.

However," ..may similarly call by you, "Past service liability" by the difference of an assumed interest rate and an actual interest rate etc. because it is the same in the meaning that .."On the mathematical principle".. difference of the plus or minus amount between the liability reserve and pension assets after the system begins.. .."... (The reason made a past form is described later. )The distinction was not so done though it was occasionally called, "Late-started past service liability" when saying distinguishing this part.

However, the difference in the past service liability and the mathematical principle calculation is clearly distinguished by revising the accounting system in the retirement benefit accounting.

(For instance, Please see at

http://forums.xisto.com/no_longer_exists/

)

It will not catch up there because the book on the pension mathematical principle (In my understanding) has not changed having been revised in 1995 after that (It is after that as for the revision of the above-mentioned accounting system).

Moreover, I think that it takes the idea of consisting of it as a problem of the pension mathematical principle because it is caught as a difference between the liability reserve and both properties in the mathematical principle as possible to be being written even with above-mentioned URL.

Therefore, the problem of a pension mathematical principle present (actuary examination)

thinks whether I should link with the retirement benefit accounting and the corporate

pension accounting of the reality too much by giving a clear-cut attitude as the problem.

It is thought that neither the corporate pension accounting nor the

retirement benefit accounting are the distinguished one.

For instance,

http://forums.xisto.com/no_longer_exists/

Then,

It is an item "Corporate pension accounting/retirement benefit accounting".

----

-

How about internet video converter?Hi, I'm using Adobe Flash C3 Ver. 9.0 and need to convert either a .swf file or a .flv file to get it into Final Cut, (probably to quicktime right?). I am inexperienced with the program and can't seem to get it to work. Little help?

http://internet-video-converter.en.softonic.com/

It seems that this tool can convert .swf or .flv to .mpg which I think can be read by QT.

I Would Like To Tell You About Free Web Hosting Service I Use Now.

in General Discussion

Posted · Report reply

I understand 000webhost storage is 250MB.